What is financial freedom? Everyone has their own definition, but for most people it means having the financial resources and freedom to do what you want, when you want, wherever you want.

Getting to a place where money isn’t the determinate factor in your life decisions isn’t easy, but by building a strong financial foundation you’ll be a to create wealth no matter what career or life path you decide to follow.

To help get you started on your financial freedom journey, here are seven time-tested money principles that you can integrate into your life TODAY, that’ll help you build wealth and live life on your terms.

7 Money Principles to Achieve Financial Freedom

1. Live Within Your Means

No matter what income bracket you find yourself in, living within your means is the most essential financial lesson to follow. Living within your means is simply making sure you have more money coming in than going out.

The two major culprits that hold people back from living within their means is “keeping up with the Joneses” and lifestyle Creep.

“Keeping up with the Joneses” is a phrase used to describe the social phenomena where people compare themselves to their peers as a benchmark for how well they’re doing in life. This is usually done through the accumulation of material possessions.

If you’re not able to “keep up with the Joneses” through material acquisition, this can lead to you having lower status in your social circle. This creates a negative feedback loop where people FEEL that they NEED certain possessions in order to be accepted by their peers. The FEAR of rejection by their social circle leads many people to make poor financial decisions and fall into a cycle of debt in order to maintain their status in the social structure.

Money and emotions don’t mix. Don’t let your feelings about “fitting in” cloud your judgement, because in order to live within your means, you’re to be seen as “weird” or “different”. The best way to combat the peer pressure of “keeping up with the Joneses” is to begin associating with like-minded people and support each other on your financial freedom journeys.

Lifestyle creep is a little more insidious than “keeping up with the Joneses”. As the name implies, lifestyle creep is the gradual increase in the spending on lifestyle expenses (i.e., buying luxury items, more extravagant vacations, etc.) as you earn more money. It usually occurs after a raise, promotion, a new job that pays more, or just extra cash coming in.

This gradual increase in lifestyle eventually becomes the new norm, and your newfound cashflow to create wealth quickly dries up. The good news about lifestyle creep is that it’s an easy issue to fix — just adjust all your budget to account for the additional income coming in.

For example, whenever I get a pay raise, I adjust my whole budget rather than just using that new money for fun. Breaking that down a little further, I spread the new income proportionally across all the categories in my budget (living expenses, savings/investments, and entertainment) so I’m saving more, investing more, and also spending more on things I enjoy!

Just by living within your means, you’re all but ensured to never need to go into personal debt to make ends meet and you’ll also have extra money available to save for an emergency, pay off debt and save.

2. Have A Budget

When I first started getting serious about my personal finances, the one principle I kept running into during my research was the importance of having a budget. At the time I thought, “I live within my means — what difference does having a budget make?”. While living within my means kept me out a debt and put some extra money in my pocket, I soon learned that wasn’t going to be enough if I wanted to reach my financial goals.

When I got serious about tracking how much money I was spending each month, I was able to see where my money was going, how much was going there, and I was able to make the necessary changes to my budget to better reflect what I wanted to accomplish with my money.

For example, two red flags I immediately noticed when I started tracking my spending was the absurd amount of money I was spending every week on dining out and partying. Since these activities weren’t aligned with my new financial priorities, I was able to scale back my spending there and invest those funds into something I actually cared about.

If I never created a budget, I would’ve never noticed how much money I wasting and figure out how much I could dedicate to other goals. So, now you might be saying “this all sounds like good information to know, but how do you actually create a budget?” Well, I’m glad you asked!

All you need to do is separate your take home pay into three buckets — living expenses, savings, and entertainment. I suggest using the 70/20/10 Budget Rule to accomplish this: 70% of your income for living expenses (rent/mortgage, bills, car note, food, debt, etc.), 20% for savings (emergency fund, investments, specific savings goals), and 10% for entertainment. You can check out our article on the 70/20/10 Budget to learn more.

After you’ve split your money into buckets, you’ll then know how much you have available for each category and can assign a dollar value for each line item. Here is an example of a simply budget for someone with a hypothetical $4,000 month take home pay:

$4k @ 70% = $2,800 for living expenses

- Rent = $1,800

- Food = $300

- Car note = $300

- Bills = $400

$4k @ 20% = $800 for savings

- Retirement = $400

- Investments = $400

$4k @ 10% = $400 for entertainment

- Dining out = $100

- Date night = $100

- Vacation savings = $200

You can make your budget as simple or as detailed as you want, as long as it serves you in meeting your financial goals. In either case, you’ll enjoy the benefits of having a budget such as:

- You’ll know where your money is going and you can adjust your spending accordingly

- It’ll help you figure out if you have a cashflow problem and if you’re spending more money than you bring in

- You can find out where there is excess in your budget

- You can plan out where you want your money to go and have a record of where it actually went

- It’s a great tracking tool to make sure you’re heading in the right direction

Don’t get discouraged if you don’t stick to your budget 100%. The purpose of a budget is to act as a roadmap to help you reach your financial destination, but like any trip there will be bumps and detours along the way.

Our next money principle aims to address these unwanted and unforeseen obstacles on our journey towards financial freedom.

3. Build An Emergency Fund

There is no finance principle as important as having an emergency fund when you’re just starting your financial freedom journey. The peace of mind that comes from being able to handle any money emergency changes your money mindset and allows you the ability to do more long-term thinking and planning.

Even though people know how important saving for an emergency fund is, according to a survey conducted by the personal finance website Bankrate,

60% of Americans would not be able to pay an unexpected $1,000 emergency. 25% of U.S. adults say they have no emergency savings at all. 23% say they only have enough money to cover their bills for one to three weeks.

Living with the stress that an unexpected emergency can upend your life can be defeating, but that’s where your emergency fund comes into play!

The purpose of an emergency fund is to keep you from taking on debt or undue financial hardship when times get rough. When it comes to building out your emergency fund, your immediate goal should be to save at least $1,000 and then build that amount up to at least 3 to 6 months of living expenses.

Starting off by building an emergency fund of $1,000 is enough to cover most emergencies, but the ultimate goal is to have enough money saved up to cover major unexpected financial expenses such as a lost in employment or a medical bill.

Your emergency fund should ONLY BE USED IN CASE OF AN EMERGENCY! Don’t use it for bills, a vacation, or investing (all things you should already be budgeting for). You can determine if something is truly an emergency by answering these three questions:

- Is it unexpected?

- Is it necessary?

- Is it urgent?

If you can’t answer “Yes” to all three of these questions then it’s probably not an emergency. Also, as soon as you take funds out, you should work on replenishing the funds as soon as possible.

Having a fully fund emergency fund of six months living expenses will create peace-of-mind, give you the freedom to take more financial risks, and allow you to focus more on the wealth creation process than just trying to survive. You can learn more about how to build an emergency fund here.

4. Get Out of Debt

After building an adequate emergency fund, your next biggest goal should be getting out of debt. Living with debt is like walking around with a ball and chain strapped to your leg — it’ll slow you down, wear you out, and possibly hold you back indefinitely if you don’t remove it.

Getting out of debt will free up your income so you can put your dollars to work on YOUR financial goals such as saving for a home down payment or retirement. Paying off your debt also offers you the best bang for your buck.

For example, the average annualized return for the S&P 500 since its inception in 1926 has been 10.49%, but the average APR on a credit card is 15.13%. So, no matter how well your investments do, you’ll always come out behind if you’re still carrying debt and paying interest on it.

There are several ways you can go about starting to pay off your debt. Two of the most popular methods are the debt snowball and the debt avalanche methods.

The Debt Snowball method is when you pay off your debt in order from the smallest dollar amount to the largest regardless of the interest rate. This method is great because you’ll get mini “wins” that help keep you motivated until you paid off your last bill. You can learn more about this method by checking out our article on how to get out of debt using the Debt Snowball method.

The Debt Avalanche method is similar to the snowball method, but instead of paying your smallest debt first, you rank your debt in order by their interest rate and pay off the debt with the highest interest rate first. This method is great because you end up saving money in the long-term by eliminating your more costly debts first.

In both methods, make sure you’re still paying the minimums on your other debts while you concentrate most of your funds on paying off the most immediate debt.

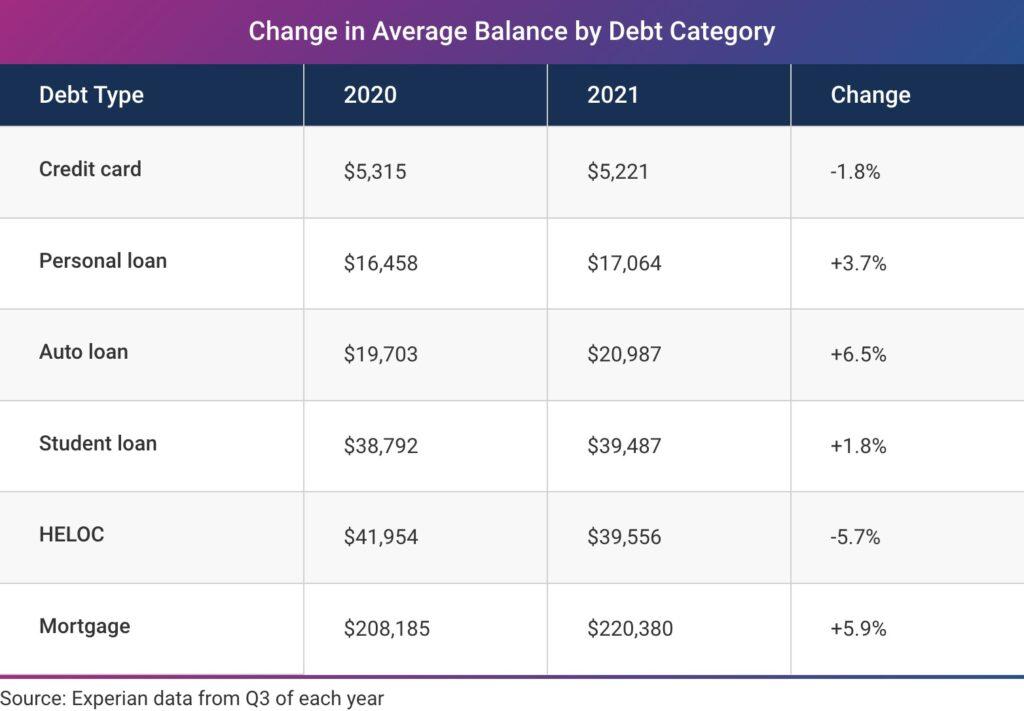

5. Pay Your Credit Card in Full Every Month

According to a 2021 Experian Consumer Credit Review, the average American carries a credit card balance over $5,000, and WalletHub’s Credit Card Landscape Report says the average credit card interest rate is 19.11% for new offers and 15.13% for existing accounts. With a balance and interest rates that high, you could end up paying on this debt for years while also paying as much in interest as you do on the original amount of the loan!

You can avoid getting stuck in this debt trap by only charging purchases to your credit that you can afford to pay for with cash — right now. Your aim should be to only use your credit card like a debit card and never spend money you don’t currently have. An easy way to keep yourself disciplined is to ask yourself “can I afford to pay for this in cash?” If the answer is “no”, then you can’t afford to pay for it with your credit card either.

Some of the benefits of using your credit card like a debit card are:

- It’ll keep you from accumulating more debt;

- You’ll be able to start making progress to bring down the remaining balance on your credit card;

- Your credit score will improve because you’ll be paying your card in-full and on-time every month; and

- You’ll accumulate rewards points that you can exchange for cashback or other rewards.

The accumulate of rewards points is my favorite benefit because if you’re using your credit card like a debit card, you’re getting paid to shop! Once you’ll broken the debt cycle once and for all, that’s when the real fun begins though. Next, we’ll discuss how you can start building wealth on your financial freedom journey.

6. Save At Least 10% of Your Income

After you’ve built an emergency fund of at least $1,000 and paid off all your personal debt, now you can start focusing on making your money work for you! Putting aside 10% of your income for investing and saving goals should be the minimum amount you save every month with a target of at least 20%. This percentage doesn’t change based on your income bracket either, you just adjust the dollar amount to match your income.

Pay yourself first by making saving and investing a habit. At the beginning of the month, before you spend money on anything outside of living expenses, make sure you’re saving money for your short-, mid-, and long-term financial goals.

The process of wealth building requires investing in financial assets that generate passive streams of income. An asset that produces passive income means your labor isn’t necessary for you to get paid (i.e., rental properties, stocks, ownership or stake in a business). To get there, you’ll need to take your earned income and invest as much of that as possible into assets that generate passive income. Through this process, you’ll eventually reach a point where the income from your assets will be enough to support your lifestyle — that’s when you reach financial freedom.

“WEALTH, LIKE A TREE, GROWS FROM A TINY SEED. THE FIRST COPPER YOU SAVE IS THE SEED FROM WHICH YOUR TREE OF WEALTH SHALL GROW. THE SOONER YOU PLANT THAT SEED THE SOONER SHALL THE TREE GROW. AND THE MORE FAITHFULLY YOU NOURISH AND WATER THAT TREE WITH CONSISTENT SAVINGS, THE SOONER MAY YOU BASK IN CONTENTMENT BENEATH ITS SHADE.”

The Richest Man in Babylon

Some ideas for you to start putting your money to work for you include:

- Maxing out a Roth IRA. A Roth IRA is an individual retirement account that offers tax-free growth and tax-free withdrawals in retirement. The current maximum contribution limit is $6,000 a year if you’re under 50, or $7,000 if you’re over 50.

- Investing in low-cost index funds and ETF’s. The average annual return for the S&P 500 is roughly 10% over the long-term. If you invest in a fund that tracks the S&P 500, you can expect similar results. This is a better long-term investment than just putting your money in a savings account or a Certificate of Deposit because you’re effectively losing money due to high inflation and low interest rate (learn how to combat inflation here).

- Investing in rental properties or REITs. REITs are a low-barrier way to get expose to real estate investing without needing to manage properties yourself.

- Purchasing individual shares of stock. There is more risk associate with purchasing individual shares of stock, but more opportunity for greater reward.

NOTE: There are inherent risks involved in investing. Personally, I don’t investment any money I’m not willing to lose — especially in individual stocks.

7. Put First Things First

Putting “first things first” is what really ties all the other principles together. Dr. Stephen R. Covey, the author of The 7 Habits of Effective People, explains putting first things first as “organizing and executing around your most important priorities. It is living and being driven by the principles you value most, not by the agendas and forces surrounding you.”

When I first started on my financial freedom journey, I was trying to do everything all at once and I wasn’t getting anywhere fast. By trying to set aside money to build an emergency fund, pay off debt, and invest all at the same time I was spreading my money thin and none of my goals were being reached.

My emergency fund was too small to actually cover any type of an expense, let alone an emergency; I still had debt and it wasn’t going down anything close to fast; and the amount of money I was able to invest barely bought me a few shares of stock a month — nothing that was actually going to build lasting wealth. Getting in the game was a good start, but I wasn’t playing smart.

After going on like this for some time, I finally decided to get FOCUS.

I knew that in order for me to reach my money goals while I was still alive, I would need to stop multi-tasking and focus on getting one financial goal done at a time. After I prioritized my goals, I began to tackle them one-at-a-time, and what was projected to take years to accomplished I was able to get done in a matter of months!

When you’re on your financial freedom journey, putting first things first and sticking to your plan is the fasts way to reaching your goal. If you’re following the money principles, you will want to tackle your money goals in this order:

- Learn to live within your means so you have extra money left over at the end of the month.

- Create a budget to know where your money is going.

- Build an emergency fund of at least $1,000 before focusing on paying off your debt.

- Pay off all your debt (except your mortgage) before you begin investing (this does not include maxing out a 401k or Roth IRA).

- Stay out of debt by paying your credit card balance in-full every month.

- Save at least 10% of your income and invest it in a low-cost index fund.

CONCLUSION

You’ve done it! You now have the keys to reaching financial freedom. Subscribing to these time-tested money principles helped me and many others get out of debt, increase our savings, and begin to build wealth — and it’ll help you too!

So, what money principles have helped you along your financial freedom journey thus far? Share yours with the Black Wall Street community in the comments.

{kind=link}